The Commercial Property Standard Questionnaire asks about anticipated VAT treatment of a transaction which may not be a TOGC, ‘however unlikely that may be’. In practice, ensuring that a transaction is properly a VAT free Transfer of a Going Concern often requires positive action to be taken.

Failing to recognise when a transaction cannot be VAT free, leaves either party to the transaction at risk of irrecoverable VAT up to 20% of the market value of the property plus financing costs and potentially penalties and interest from HMRC.

Who should attend Our update is aimed at commercial property lawyers and we will walk through all the requirements for a VAT free TOGC and highlight those transactions which cannot qualify. It will also explore practical considerations to help you understand the steps required by property owners and buyers to avoid an unnecessary VAT charge.

Key takeaways:

• When can a transaction be VAT free

• What actions and notifications are required to ensure TOGC status

• Additional considerations for Capital Goods Scheme items

• Impact if VAT is not charged when it should be

• How to prepare in good time for a TOGC property transaction

Related Videos

Investment ready: how to build a business investors trust (and buyers value)

13594 views 3 June 2026

Food in Flux: The impact of global events on the food chain | Part 1 | with Sarah Calcutt

6938 views 19 May 2026

Pensions Perspectives Episode 8 – A new pensions act is imminent! What do you need to know?

13781 views 27 April 2026

Social Housing Know How – Series 3: Fraud Prevention & Governance in Practice

5976 views 24 April 2026

Japanese Corporate Governance Explained | Early-Stage Reform & Boardroom Insights

4662 views 16 April 2026

AI strategy: does scrappy speed beat corporate caution? | Alternatively Speaking #4

8604 views 7 April 2026

HR People Pod – Ep 45: The problem with pay secrecy | Pressure-proof managers | Are PIPs broken?

5601 views 7 April 2026

What’s going to build confidence in UK real estate? | The Market in Minutes

12827 views 1 April 2026

EIS Investing Explained: Strategic Investing & Tax Planning for Company Directors

37668 views 10 March 2026

Investing and Trading with UK Tech Industries.

Do pension scheme trustees manage risk effectively?

Vodafone – Sponsors of BusinessTV

Time to talk about mental health at work

Business Negotiation Skills Training Course from the Chartered Institute of Marketing

Maximise your Export Potential

Popular

Preparing for Green Reforms: Impact on the retail sector

Mishcon de Reya LLP130008 views 18 July 2024

UK Foodstores: 5 things you should know

Knight Frank119352 views 18 March 2024

Salary Sacrifice for Pensions: Still a Powerful Tool But After the NI Changes Employers Need a New Game Plan

BusinessTV49046 views 12 January 2026

Grow your Pension, Buy Commercial Property, Invest in your Business.

BusinessTV47118 views 29 March 2025

Future-Proofing Your Wealth with Trusts and Family Investment Companies.

BusinessTV41878 views 9 December 2025

Funding the Sale of Your Business to an Employee Ownership Trust

BusinessTV40056 views 22 October 2024

Why every business needs an Active approach to Cyber Security

BusinessTV39993 views 8 June 2025

EIS Investing Explained: Strategic Investing & Tax Planning for Company Directors

BusinessTV37668 views 10 March 2026

Intellectual Property to Drive Growth, Access Funding and Improve Resilience

BusinessTV35114 views 19 January 2026

Enterprise Management Incentives: One of the best ways to retain and attract talent just got better.

BusinessTV33550 views 7 May 2026

Price Increase Management for B2B Companies

Simon-Kucher & Partners32269 views 15 March 2022

Tom Stevenson’s Q4 Investment Outlook

Fidelity UK31611 views 13 October 2022

Retailer pricing strategies

Simon-Kucher & Partners30877 views 31 August 2022

Greenification of Transport Webinar – The future of clean mobility in Europe

Fieldfisher28824 views 17 August 2022

What the new government means for business

CBI26246 views 15 July 2024

Promotion effectiveness for consumer goods companies

Simon-Kucher & Partners26075 views 19 August 2022

The Wealth Report 2022

Knight Frank25450 views 8 April 2022

Addressing the legal and tax issues for employers for hybrid and remote working

Ince25300 views 11 November 2022

Winning With Emotion: How To Become Your B2B Customers’ First Choice

B2B International Market Research25256 views 1 November 2021

Looking beyond pay to help employees

Barnett Waddingham24826 views 20 December 2022

Latest Content

What big bank share buybacks tell investors

Killik & Co9206 views 10hours ago

Renewable Energy for Farmers: Breaking Down the Complex Crossover Between Agriculture and Energy

Shakespeare Martineau3534 views 11hours ago

Investment ready: how to build a business investors trust (and buyers value)

Harper James13594 views 3 June 2026

Business impact | Employee empowerment | Change readiness in an AI world

Chartered Institute of Personnel and Development6268 views 3 June 2026

C-suite barometer 2026: Navigating economic uncertainty

Forvis Mazars10737 views 2 June 2026

2026 Top Cybersecurity Trends: What CISOs Need to Know

Gartner12939 views 2 June 2026

EY UK Economic Outlook – Spring 2026

EY UK&I16275 views 1 June 2026

2026 priorities for insurance sector

Grant Thornton8558 views 1 June 2026

Art of advice: Elizabeth Bird and Andrew Teeman on high-net worth planning and later life lending

Legal & General8283 views 29 May 2026

Dr Daniel Hulme: AI and the entrepreneur

Rathbones6153 views 29 May 2026

FutureProof: Artificially negligent?

Mills & Reeve5703 views 29 May 2026

Pension Savings Pathway, Longevity Stats Update, The Rise of the Finfluencer & More | Pensions in 10

Broadstone11587 views 28 May 2026

Understanding salary vs dividends

Azets UK8296 views 28 May 2026

Semafor World Economy Summit: Greg Case on Geoeconomics of AI

Aon3508 views 28 May 2026

The value of trade marks – IPO meets the British Brands Group

Intellectual Property Office UK6202 views 27 May 2026

Tokenisation and trust

HSBC9259 views 26 May 2026

How to find your voice and keep imposter syndrome under control

The Chartered Institute of Marketing4435 views 26 May 2026

Talking Heads – Flows into core equity ETFs hold up amid Middle East conflict

BNP Paribas Asset Management5586 views 22 May 2026

How leaders sustain momentum and protect their people in an era of transformation overload

PA Consulting13532 views 22 May 2026

The UK Crypto Regime — Why Firms Need to Move Now

Latham & Watkins7316 views 21 May 2026

Trust in AI Is Falling…What Happens Next?

Gartner9486 views 21 May 2026

Breaking down the walls on giving clarity to customers, and confidence to advisers

Legal & General4134 views 20 May 2026

Don’t get caught out: 2026 Employment Law update

IOD6922 views 20 May 2026

The IP Driven Start-up: Episode 3 – Why deep-tech ventures can fail

Marks & Clerk14468 views 19 May 2026

Food in Flux: The impact of global events on the food chain | Part 1 | with Sarah Calcutt

MHA UK6938 views 19 May 2026

Global private equity report 2026: Matthieu Boyé and Scott Linch

Forvis Mazars6882 views 19 May 2026

Apprenticeships Explained: What’s Changed and What It Means for Employers and Apprentices

Make UK - The Manufacturers' Organisation10692 views 18 May 2026

The Role of Grid Connections in Planning Applications

DLA Piper5440 views 18 May 2026

Performance and VFM & Ping-Pong! | Pensions in 10

Broadstone8822 views 15 May 2026

How do we turn AI ambition into a national advantage?

Deloitte3509 views 15 May 2026

Four generations, one workplace. Clash or catalyst? | Alternatively Speaking #5

Grant Thornton8354 views 14 May 2026

Perspectives: Beyond the dollar

HSBC15100 views 14 May 2026

Pension contributions as you approach retirement

Legal & General6324 views 13 May 2026

Commercial growth in a fragmented world

Simon-Kucher & Partners8296 views 13 May 2026

Beyond the bot: Scaling AI agents across the enterprise

Capgemini11457 views 12 May 2026

Taking Stock – After The Bell: Money on Your Mind

Quilter Cheviot4740 views 12 May 2026

Scaling SaaS videos: SaaS valuations explained

Moore Kingston Smith LLP5276 views 11 May 2026

What’s going to build confidence in the UK Rural real estate sector?

Savills8320 views 11 May 2026

Double tax? 9 steps to tackle the IHT change coming for your pension

Fidelity UK8233 views 8 May 2026

SPP Beginner’s Guide to Pensions Fraud and Scams

The Society of Pension Professionals4518 views 8 May 2026

Enterprise Management Incentives: One of the best ways to retain and attract talent just got better.

BusinessTV33550 views 7 May 2026

Protecting portfolios | Investment Update, April 2026

Rathbones11135 views 6 May 2026

What do the Middle East developments mean for UK businesses?

PwC14365 views 6 May 2026

What makes AI and digital transformations fail commercially?

Simon-Kucher & Partners8591 views 5 May 2026

How is real estate managing climate risk at scale?

Jones Lang Lasalle5001 views 5 May 2026

Perspectives: Energy shocks and security

HSBC10743 views 1 May 2026

The IP Driven Start-up: Episode 2 – What investors really look for

Marks & Clerk13006 views 1 May 2026

What’s Next for Manufacturing? | Stuart Weekes Talks with Jonathan Dudley

Crowe UK12682 views 30 April 2026

The big April 2027 pensions rule change

Killik & Co8425 views 30 April 2026

Making News – Navigating the energy crisis

Make UK - The Manufacturers' Organisation13565 views 29 April 2026

Quarterly Market Review for Charities – Q1 2026

Rathbones7252 views 29 April 2026

Raising standards of trusteeship and governance

The Pensions Regulator10763 views 28 April 2026

How the next wave in AI will transform market infrastructure

Oliver Wyman7077 views 28 April 2026

Pensions Perspectives Episode 8 – A new pensions act is imminent! What do you need to know?

Willis Towers Watson13781 views 27 April 2026

Food & Agribusiness AM: breakfast briefing session

Mills & Reeve5251 views 27 April 2026

Let’s talk antitrust | The online food delivery cartel

Norton Rose Fulbright8457 views 24 April 2026

Pensions Bill, Triple Lock Speculation & Fresh Calls for Contribution Hikes | Pensions in 10

Broadstone11685 views 24 April 2026

Social Housing Know How – Series 3: Fraud Prevention & Governance in Practice

Menzies5976 views 24 April 2026

From searchless retail to AI decision‑making | Agentic commerce

Capgemini8371 views 23 April 2026

Very important: Inheritance Tax UK rules may change in 2026 — most people aren’t prepared

Bluebond6729 views 23 April 2026

Treat the business of sustainability like any other business

The Carbon Trust6917 views 22 April 2026

The European Battery Energy Storage System (BESS) economy

Fieldfisher11836 views 22 April 2026

Agriculture and Planning Experts Discuss Natural Capital for Farmers

Shakespeare Martineau3301 views 22 April 2026

Smart investors use these investments for income – here’s how

Fidelity UK9397 views 21 April 2026

What’s the biggest shift in UK public sector tech procurement?

BaringaPartnersLLP5976 views 21 April 2026

The IP Driven Start-up: Episode 1 – the real story of commercialising university research

Marks & Clerk8473 views 20 April 2026

Real Estate in 2026: Trends, Risks and Opportunities

Grant Thornton16109 views 20 April 2026

Your workplace pension – the easiest way to build wealth?

Legal & General6378 views 17 April 2026

Growth to withstand Mid East conflict | Monthly Investment Insights

Zurich Insurance Group13637 views 17 April 2026

The new unfair dismissal era What employers must know

HR Solutions8361 views 17 April 2026

Japanese Corporate Governance Explained | Early-Stage Reform & Boardroom Insights

IOD4662 views 16 April 2026

Is AI eroding creativity?

The Chartered Institute of Marketing14685 views 16 April 2026

The Macro Brief – Tracking economic disruption

HSBC11571 views 15 April 2026

Economy and investment webinar – March 2026

Forvis Mazars10773 views 15 April 2026

Tuned in: How customer listening creates actionable insights

Huthwaite International7662 views 15 April 2026

Customers Don’t Reject AI…They Reject Being Dehumanized | Gartner CIO Leadership Forum

Gartner17090 views 14 April 2026

What does the UK’s new Employment Rights Act mean for your business?

Saffery12854 views 14 April 2026

SPP Insights: Private Market Investment

The Society of Pension Professionals6414 views 14 April 2026

Data Center Insights – Leasing Data Centers in a Fast-Moving Market

Latham & Watkins8358 views 13 April 2026

Fake reviews and pricing under the DMCCA spotlight

Gowling WLG13057 views 10 April 2026

How to make your cash reserves work harder

Killik & Co8317 views 10 April 2026

The Sovereign Sessions: Enforcement against sovereigns

Norton Rose Fulbright4974 views 9 April 2026

Emma Vaughan | Protection from every angle: Never compromising on the safety net

Legal & General6636 views 9 April 2026

Taking Stock – After The Bell Podcast: A Candid Conversation with the QC CEO

Quilter Cheviot6042 views 8 April 2026

Salary Sacrifice Cap, Transition Pathways & Impersonation Fraud | Pensions in 10

Broadstone13589 views 8 April 2026

AI strategy: does scrappy speed beat corporate caution? | Alternatively Speaking #4

Grant Thornton8604 views 7 April 2026

HR People Pod – Ep 45: The problem with pay secrecy | Pressure-proof managers | Are PIPs broken?

Chartered Institute of Personnel and Development5601 views 7 April 2026

AI in Banking at executive level: Governance, safety and the future of work (ING COO/CTO)

ING4101 views 6 April 2026

Understanding the New Trustees’ Annual Report Requirements | SORP 2026 Explained

UHY Hacker Young5039 views 6 April 2026

Investment Insights Webinar – Q1 2026

Rathbones15480 views 2 April 2026

COO Network podcast – The tyranny of the urgent: How COOs stop the firefighting loop

BaringaPartnersLLP13770 views 2 April 2026

The 2026 macro reset: Energy price hikes | What’s brewing? With Matt and Guy

Zurich Insurance Group18640 views 1 April 2026

What’s going to build confidence in UK real estate? | The Market in Minutes

Savills12827 views 1 April 2026

How Brand Research Drives Smarter B2B Acquisitions with Trevor Glue, Marketing Director at Ricardo

B2B International Market Research8759 views 1 April 2026

Smarter energy management in 2026

Duncan Toplis6478 views 31 March 2026

Talking Heads – Electrification and AI turbocharge clean energy outlook

BNP Paribas Asset Management5339 views 31 March 2026

Pension Scams Action Group webinar: Join the fight against pension fraud 2026 v1.0

The Pensions Regulator11773 views 30 March 2026

RIPE | Employment Rights Act: what’s next?

Freeths7357 views 30 March 2026

Spring Meetings: What Trustees Need to Know | Pensions in 10

Broadstone5858 views 27 March 2026

The ‘set-and-forget’ funds I’m buying for the next decade

Fidelity UK7813 views 27 March 2026

AI Unscripted bonus episode – 2026 AI Business Predictions

PwC8562 views 26 March 2026

Brand Vulnerability: What does the world see when they look at your Domain Name

Thames Valley Chamber of Commerce12855 views 26 March 2026

Why internal buy-in makes or breaks deals | Mastering Sales & Negotiations

Huthwaite International10017 views 25 March 2026

The ORA Journey: lessons, tips, and the road ahead for Own Risk Assessment

Barnett Waddingham6428 views 25 March 2026

SRS and what it means for UK business: a practical briefing

Saffery10798 views 24 March 2026

No APIs, No AI: How Software Engineering Must Change

Gartner8415 views 24 March 2026

Helping you understand the FCA’s 2026 rules on non‑financial misconduct

Grant Thornton6843 views 23 March 2026

SPP Beginner’s Guide to Investment

The Society of Pension Professionals5099 views 23 March 2026

HR People Pod – Ep 44: Crisis leadership | Impact of employee benefits | Friction-maxxing at work

Chartered Institute of Personnel and Development5596 views 20 March 2026

12 basic tips for investors

Killik & Co6431 views 20 March 2026

Make UK National Manufacturing Conference 2026 – Economic Keynote speech by Jon Sopel

Make UK - The Manufacturers' Organisation11578 views 19 March 2026

From attention to experience: The latest shift in brand strategy

The Chartered Institute of Marketing6608 views 19 March 2026

AI for Charities: Practical applications, risks and opportunities

Rathbones4914 views 18 March 2026

Understanding share-based payments

Azets UK6690 views 18 March 2026

Market update: navigating another year in the ‘Turbulent Twenties’

Canaccord Wealth8669 views 17 March 2026

Navigating global talent: How UK businesses attract, move & retain talent worldwide

Moore Kingston Smith LLP7464 views 17 March 2026

People Matter: Settlement

Mills & Reeve5241 views 17 March 2026

How to mitigate evolving risk and keep pace with regulation

PwC8282 views 16 March 2026

Premium Bonds: who should buy them – and who shouldn’t?

Fidelity UK9302 views 16 March 2026

RE-imagine Real Estate: Ep.2-SEA & Malaysia Property Outlook 2026 | JLL

Jones Lang Lasalle3769 views 16 March 2026

Investigations: Finding Clarity, Not Certainty

Grant Thornton6359 views 13 March 2026

The Pensions Risk Transfers – 2026 market outlook

Legal & General8384 views 13 March 2026

Market Update Q1 2026

Gardiner & Theobald8566 views 12 March 2026

Outline Webinar: The Planning and Infrastructure Act 2025

DLA Piper6415 views 12 March 2026

Pensions Perspectives Episode 1: UK Autumn Budget 2025

Willis Towers Watson6382 views 11 March 2026

Exporting to the EU in 2026: VAT Changes & Regime 42

Thames Valley Chamber of Commerce11945 views 11 March 2026

EIS Investing Explained: Strategic Investing & Tax Planning for Company Directors

BusinessTV37668 views 10 March 2026

Key changes to inheritance tax: What family businesses need to know

Moore Kingston Smith LLP16444 views 10 March 2026

Breaking Ground: 2025 building safety round up

Mills & Reeve6762 views 10 March 2026

The Sovereign Sessions: Managing sovereign risk

Norton Rose Fulbright4550 views 9 March 2026

AMATS 2025 Reflection and 2026 Outlook

Aon10886 views 9 March 2026

Is a crisis mindset holding businesses back? | Alternatively Speaking #3

Grant Thornton12036 views 6 March 2026

Taking Stock – After The Bell Podcast: Bricks over Bytes

Quilter Cheviot6378 views 6 March 2026

FRS 102 – understanding changes in financial reporting

Saffery9818 views 6 March 2026

Financial Education | Pensions in 10

Broadstone8400 views 5 March 2026

Training should not be a tick-box (Root Cause Analysis – Episode 17)

Make UK - The Manufacturers' Organisation4513 views 5 March 2026

The LathamTECH Podcast: Trade Secrets — The New Litigation Battleground

Latham & Watkins9457 views 4 March 2026

SPP A Beginner’s Guide to AI in Pensions

The Society of Pension Professionals5431 views 4 March 2026

Optimising the UK prudential framework: Basel 3.1 and beyond

PwC10578 views 3 March 2026

Why investors may rue the return of “Off Balance Sheet Finance”

Killik & Co7802 views 3 March 2026

Zero-Rated & Exempt – VAT Myths

Price Bailey5842 views 2 March 2026

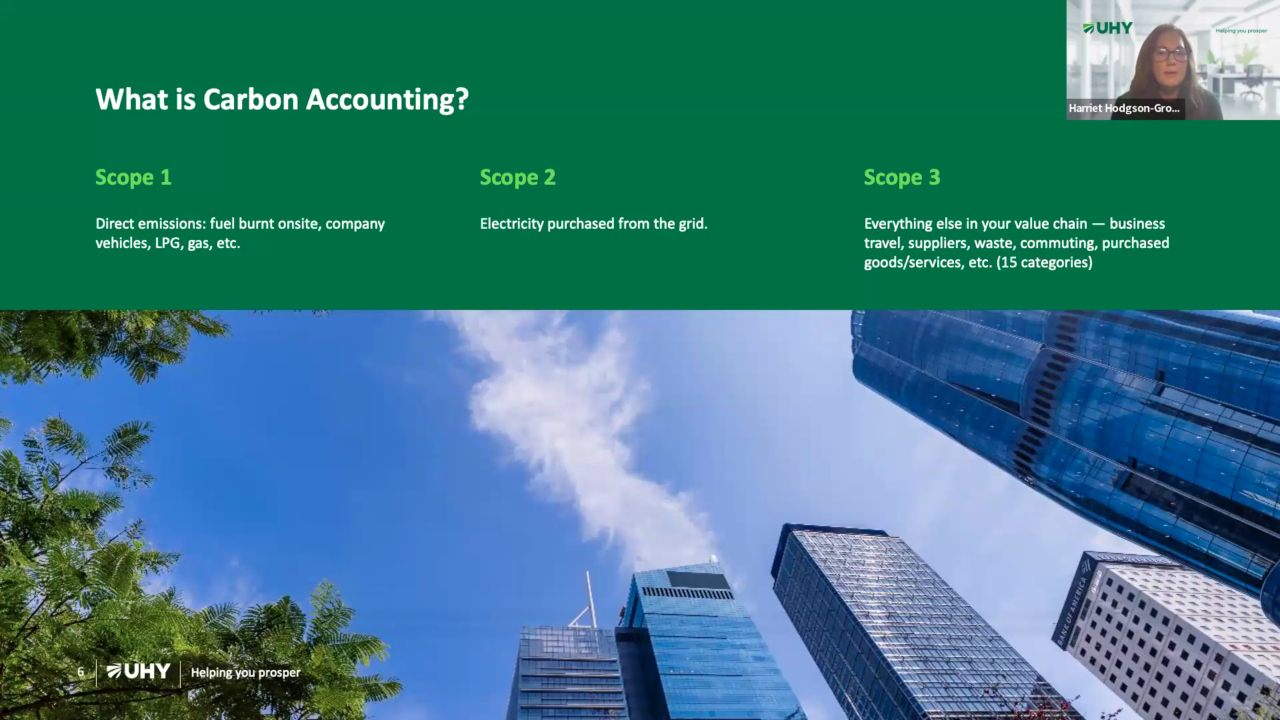

Helping you prosper: Turning carbon reporting into a business opportunity

UHY Hacker Young4013 views 2 March 2026

Understanding changes to UK GAAP

Azets UK9338 views 27 February 2026

Selling your agency: Turning AI capability into agency value

Moore Kingston Smith LLP7749 views 27 February 2026

CIPD’s Reward survey: Focus on employee benefits 2026 report

Chartered Institute of Personnel and Development13417 views 26 February 2026

Preparing for the Employment Rights Bill – What Employers Need to Know

Henderson Loggie4496 views 26 February 2026

Global paradox: Geopolitical bluster & booming financial markets | What’s brewing? With Matt and Guy

Zurich Insurance Group11684 views 25 February 2026

ECCTA compliance series: Risk Assessment

Fieldfisher3542 views 25 February 2026

The double negotiation: the art of the internal and external deal | Mastering Sales and Negotiations

Huthwaite International7593 views 24 February 2026

Space X buys Xai, a new boss for Disney and why NS&I premium bonds are so popular

AJ Bell6417 views 24 February 2026

2026 financial services regulation trends to watch

EY UK&I12943 views 23 February 2026

IT Operations Are Not Ready for AI Agents: How to Respond Today

Gartner5493 views 23 February 2026

Taking Stock – After The Bell Podcast: Dog on a Lead

Quilter Cheviot8603 views 20 February 2026

Let’s talk antitrust | The Nissan Iberia case

Norton Rose Fulbright4500 views 20 February 2026

COO Network podcast – COOs as translators: Bridging the boardroom and the business

BaringaPartnersLLP9220 views 19 February 2026

BS EN ISO 14001:2026 Environmental Management Systems: What’s New?

British Standards Institution (BSI Group)6700 views 19 February 2026

The fundamentals of Customs & Duty

Azets UK12566 views 18 February 2026

Regulatory Initiatives Grid & Risk Transfer Market | Pensions in 10

Broadstone5429 views 18 February 2026

Why don’t UK investors like UK companies?

Fidelity UK11665 views 17 February 2026

CFAAR Panel Special – Global Warming or Another Crypto Winter?

Grant Thornton5366 views 17 February 2026

The creative strategies defining brand success in 2026

The Chartered Institute of Marketing6716 views 16 February 2026

Mastering VAT Recovery: Process, Pitfalls & Practicalities

Saffery10769 views 16 February 2026

US dollar forecast 2026: Stable or stormy? | Monthly Investment Insights

Zurich Insurance Group11863 views 13 February 2026

How to plan for the new tax year

Moore Kingston Smith LLP16670 views 13 February 2026

Transforming IT Operations in the Era of AI Agents

Gartner8797 views 12 February 2026

eATA 2026: Navigating the Transition to Digital ATA Carnets

Thames Valley Chamber of Commerce6904 views 12 February 2026

A landmark report to guide financial institutions through emerging legal and regulatory challenges

A&O Sherman12775 views 11 February 2026

Finance Leaders Barometer – Public Sector Results

Grant Thornton8485 views 11 February 2026

Is it time to reset supply chains?

Deloitte11357 views 10 February 2026

Employment Rights Act Webinar

Menzies6748 views 10 February 2026

Winter webinar: Unwrapping investment opportunities for 2026

Canaccord Wealth10883 views 9 February 2026

Clean Tech and AI

Withers & Rogers6154 views 9 February 2026

Six investing red flags (from the private credit world)

Killik & Co11746 views 9 February 2026

FT’s Jonathan Guthrie: this is the truth about investing

Fidelity UK15706 views 6 February 2026

Building foundations in a world chasing what’s next: HR People Pod – Ep 41

Chartered Institute of Personnel and Development6741 views 6 February 2026

Food & Agribusiness AM: Sustainability regulations – what food producers need to know

Mills & Reeve5044 views 5 February 2026

CharitEpulse: Diversity, disclosure and debt

Moore Kingston Smith LLP3479 views 5 February 2026

Let’s talk antitrust | Economic growth, UK merger control reforms

Norton Rose Fulbright9195 views 4 February 2026

HMRC enquiries: what to expect and how to prepare

Saffery11751 views 4 February 2026

EMEA Real Estate Outlook 2026

Jones Lang Lasalle12041 views 3 February 2026