We chat with Elissavet Grout, Partner – Tax Incentives and Remuneration Group – at leading Law Firm Travers Smith, to discuss Enterprise Management Incentives. EMIs, which have long been one of the best ways for companies to retain and attract key talent, are now available to a much larger number of companies thanks to HMRCs recent expansion of their qualifying criteria. Key changes include doubling the employee limit to 500, quadrupling the gross assets limit to £120 million, raising the individual option limit to £6 million, and extending the maximum exercise lifespan to 15 years.

Q1. Could you take us all through exactly what these are. Give us an overview, please?

Q2. Is 50% outside ownership the difference between a company being viewed as independent?

Q3. What exactly does ‘granting an option’ mean?

Q4. Why are EMIs, considered by so many businesses to be such an attractive way of incentivising staff, Elizabeth?

Q5. Do employees typically understand all of these benefits that are going to come their way?

Q6. And from the employer’s perspective, where is the value?

Q7. How typically are the advantages of EMIs communicated to employees?

Q8. What will be the effect of the recent expansion of EMI schemes?

Q9. Why do you think this expansion of EMI was not implemented sooner?

Q10. Will those larger, more established businesses be interacting and using EMI in the same way that smaller businesses have done historically?

Q11. What key elements does a well planned EMI Scheme need to contain?

Q12. And I take it you and your team, Elissavet, are holding your client’s hands through that process?

Q13. Could a poorly drafted EMI Scheme negativity effect a business exit or sale?

Q14. How critical are accurate valuations to the long term success of an EMI scheme?

Q15. Are there any compliance or administrative issues that can raise their heads after an EMI scheme has been implemented?

Q16. Do you see any common denominators between companies who are who are entering into EMI?

Q17. If EMI is not the best choice for a company can you advice on other types of incentives and remunerations?

Q18. When should individual business owners get in contact with you and your team?

Q19. Is there any jeopardy involved when deciding which employees are going to be offered EMI?

Q20. Any, any other sort of key pieces of advice that you would give potential EMI adopters?

Important Notice

All the changes to EMI that have come into effect from 6 April 2026 do NOT apply to ‘Specified Northern Ireland Companies’. For these companies the previous parameters continue to apply. A Specified Northern Ireland Company is one which has a registered office in Northern Ireland and carries on a trade involving either a trade in goods or the generation, transmission, distribution, supply, wholesale trade or cross-border exchange of electricity.

Important Notice

All the changes to EMI that have come into effect from 6 April 2026 do NOT apply to ‘Specified Northern Ireland Companies’. For these companies the previous parameters continue to apply. A Specified Northern Ireland Company is one which has a registered office in Northern Ireland and carries on a trade involving either a trade in goods or the generation, transmission, distribution, supply, wholesale trade or cross-border exchange of electricity.

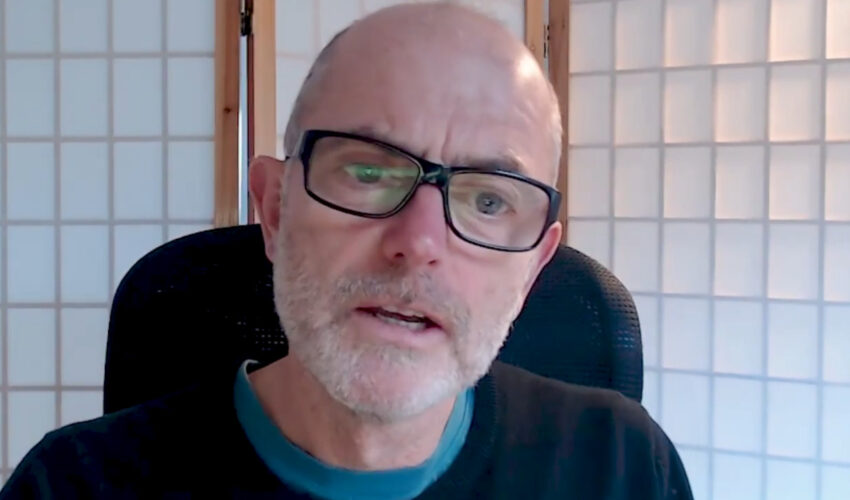

Marc Harris: BusinessTV

Thanks very much for joining us. Nice to see you again.

Elissavet Grout: Travers Smith

You too, Mark.

Marc Harris: BusinessTV

Thank you. Thanks. So a lot of companies, for reasons that will unfold later on in the conversation, will be coming to enterprise management incentives for the first time. So perhaps you could just sort of take us all through exactly what these are. Give us an overview, please.

Elissavet Grout: Travers Smith

Yes, of course. Now, in a nutshell, enterprise management incentive plans or options are a tax-favoured share option arrangement, which were originally designed for small to medium-sized companies in a high-risk trading activity. And there are many, many conditions that these companies have to satisfy before they can qualify to grant what we call EMI options. And we’ll touch upon these in our discussion as we go through everything. But there are a few points to note right at the beginning when a company is looking to this regime to see whether they can qualify. And one very key point that everyone needs to be aware of is that they are only available for companies that are independent. And we often refer to this as the independence test. And what that means is that the company that’s looking to grant the EMI options can’t be controlled by another corporate, so another company. And this is usually the case for founder and startup businesses. But sometimes when second and third round levels of investment come in, they might come in from a private equity house. And if that private equity house takes a controlling interest in your business, then you are deemed to be controlled by a corporate, which would make you ineligible for EMI options going forward. So the independence test is quite important. And unfortunately, it’s not just that you can’t be controlled by a corporate. That’s test one, I suppose, condition one. There also can’t be any arrangements under which you could come under the control of another corporate. And that’s the second limb to this test. And that can sometimes catch people by surprise or cause issues as a company grows and is looking perhaps to bring on more investment or maybe sell itself and thinking about, well, let’s grant some options now before that happens. Well, there is a threshold that HMRC will look at and consider whether or not you are in fact in a situation where you could come under control of another corporate. So the independence test is the first test that you need to look at when you’re thinking about EMI. The second very obvious test is the trading activities. So companies that want to take advantage of EMI have to be trading or preparing to trade. And the types of trading activities that are acceptable for this regime are specified in the legislation. And there are certain trading activities that are excluded. And those include banking and financial services, property development, hotel management, and certain leisure industries, as well as the provision of certain services, including legal and accountancy services. So those two key points, independent and trading.

Marc Harris: BusinessTV

Obviously, for most private companies and family businesses, when we’re talking about an outside, for example, private equity firm being involved, that control is going to materialise if they own more than 50% of the business. So I’m assuming that under 50% of the business, then a company would still qualify as independent. So perhaps that’s the first question. Is that correct, just for clarity?

Elissavet Grout: Travers Smith

That is usually the case, but does need to be considered with legal advice. Because as I said, there might be arrangements where that investor might have rights to step in and take control at some point in the future, or it might have rights where it can determine what the business does in its day-to-day activities. And again, from HMRC’s point of view, there’s a threshold above which you tip into being non-independent, even if from a share capital point of view, you don’t have more than 50%, you still may be deemed to have sufficient control to fail these EMI conditions. So if you are in that situation, it certainly requires some careful thinking.

Marc Harris: BusinessTV

When it comes to the term or the process of granting an option, can you just sort of clarify for us what that means? Because I think that’s an important point because company owners, of course, don’t want to be giving away or feel that they’re giving away control of their business on day one. So can you sort of clarify for us exactly what granting an option means?

Elissavet Grout: Travers Smith

Of course, yes. So this is the beauty of options. They are contractual agreements between the two parties that at some point in the future, if certain conditions are met, including quite importantly, the continuing to be an employee, you will have the right to buy shares in the business at a predetermined price. So you fix the price on day one, and you say to an individual, subject to all of these terms and conditions on a particular date or on the occurrence of a particular event, you have the contractual right to call on us to give you shares in our business. But during that period, some people call it vesting period or option period, you just have a contract. You do not have rights to the shares underlying that contract. You do not have voting rights, and you do not have dividend or other economic rights in relation to those shares. So typically, you don’t have to ask your option holders for consent if you want to do something as a business because they’re not shareholders. So they will though, these options have a dilutive effect ultimately. So you do as a shareholder and a cohort of shareholders need to think about, well, how much dilution am I happy to live with when the time comes? How much value of my company do I want to give away? Do I want to cap the level of returns that individuals receive? What conditions do I want to add to these options that I am comfortable with from a commercial perspective? And there are potentially consents that you have to get from certain shareholders because your shareholders agreement might require that. Under the Companies Act in the UK, if you’re incorporated in the UK, there are certain exemptions from having to get authority to a lot and grant the options or a lot of the underlying shares. But it requires a little bit of maybe 10 to 15 minutes of just checking all those constitutional documents so that you understand how you can go about this. But in effect, it’s a contractual agreement between the two parties and it’s not the issue of shares at grant.

Marc Harris: BusinessTV

Why are Enterprise Management Incentives, EMIs, considered by so many businesses to be such an attractive way of incentivising staff, Elizabeth? Perhaps you could sort of speak to that in general terms and perhaps also specifically as it might relate to the employment landscape at the moment, which is of course quite challenging.

Elissavet Grout: Travers Smith

Yes, of course. I mean, and even when these were originally introduced quite a while back now, they were introduced for companies which didn’t really have much cash flow. So when they were looking to recruit or even retain their key talent, they didn’t really have the ability to pay high salaries or large cash bonuses. And stock essentially is quite cheap because you’re not putting any money down. And ultimately the value that the individual realises for that stock will be at a liquidity event in the future and most likely either from a purchaser of the business. So you’re not putting down that cash. So it’s very cash flow friendly. And when you’re in a startup environment or even a growing environment, that’s quite important to people. Certain industries also in the tech space, especially when compared to the States, it was quite customary in the States to give stock options to people. And that kind of filtered through into the UK market in those tech industries. And so there was an expectation of employees that when they’re looking to start a position somewhere in a tech company, that stock options would be part of their package. So there’s a cultural expectation in those industries, but it’s also very cash flow friendly. But in terms of the UK environment in particular and the tax environment we have in the UK, the main benefit of an EMI option is that if all goes well and all the conditions are met and continue to be met, you will be taxed and treated as a taxpayer in the capital regime. So not the income regime, which applies to your salary and your bonus, but the capital regime, which applies to the purchase of assets. And in the UK, we have very, very different rates for those two. So our salaries and benefits are taxed at 45%. That’s the highest rate that you could be taxed at. And employees have to pay 2% employee national insurance contributions. So a combined rate of 47%, if you’re a high earner. And these days, it’s not really even that high, that threshold, or 42%, if you’re the majority of people are in that bracket. And in addition, our salary and benefits are subject to employer’s national insurance contributions. And over the last few years, we’ve seen that increasing over time. It’s currently at a rate of 15%. So you’ve got an extra cost of 15% on top of anything you want to give your employees to remunerate them. And all of those taxes are also subject to payroll. So that means the employer is responsible for withholding those taxes and paying them to our tax authorities. So there’s an added burden of compliance in that respect. Compared to capital treatment, our capital gains tax rate is currently 24%. It’s a very big difference between the income rates of 40 or 45. There’s a small annual exemption of £3,000 currently. Historically, that was as high as £12,000 or more, so it was even better in years gone by. But still, the 24% rate is great. And there is no employer national insurance contributions or employee national insurance contributions on capital gains. So immediately the business and the employee is saving a lot of tax. And there are even more beneficial rates for EMI option holders if they hold their options for at least two years before they exercise them and sell the underlying shares, you can get business asset disposal relief rates, which are even more generous. They’re going to be 18% from April. And so instead of 24, you’re at an 18% rate, which again is excellent compared to the income tax rates. So that really is the kind of the tax favoured aspect of EMI. So even though commercially EMI options make sense and the businesses require them, the fact that they have these amazing tax benefits associated with them just make them very attractive to businesses that can qualify to grant them.

Marc Harris: BusinessTV

Do employees typically understand all of these benefits that are going to come their way?

Elissavet Grout: Travers Smith

I think I think a well-designed plan and a well-communicated plan can have can land really well with your employee population. And it’s key to all of incentivisation giving, you know, you spend a lot of legal fees, valuation fees, you know, admin fees on producing and preparing plans like these. But if they don’t get received very well, then you’ve kind of wasted your time. So there is a communication piece to kind of make people understand the benefits. I think a lot of people now, you know, when they move jobs, they are used to these arrangements. And so they are looking for them. They’re looking to replicate them in a new job that they might go to. So it can be led by the employee themselves saying, oh, by the way, in my previous job, I had this benefit. Can I, you know, can I have the same here with you? So there is sometimes you see employees asking for these. So, yeah, I would say typically once the tax benefits are explained, it becomes a no brainer from an employee perspective.

Marc Harris: BusinessTV

And from the employer’s perspective, where is the value? Where is where do you find most employers perceive the value?

Elissavet Grout: Travers Smith

For employers, what they like about EMI is obviously the tax benefits, no employer national insurance contributions. You know, if you were to compare it with a non-tax favoured or we call them unapproved stock option, it would be taxed as income with payroll and national insurance contributions. And whilst an EMI option, if everything works well and as it should, won’t have that. So it’s a massive cost saving. And whilst employers could pass on the employer NICs cost to their employees and their option holders, you know, that’s not massively attractive because it increases the individual’s combined tax rate to around 55%. No one really wants to go out and sell that to their employee population. It’s not it’s not particularly a good message to give. But in addition to that, EMI is flexible. It doesn’t require you to offer the options to everyone. So you can pick and choose who you give them to. So you can use them to retain your key talent and recruit key talent rather than apply it across the board equally. Although many businesses do do that and there’s nothing wrong with that. You can have vesting criteria as you wish. You can have performance conditions as you wish. So there is a lot of commercial flexibility in using an EMI plan.

Marc Harris: BusinessTV

How typically are the advantages of EMIs communicated to employees? How does that typically happen? Does a does a does a company sort of tend to do that themselves and take sort of individual employees to a little bit of a sort of an education session on it? Or do they engage a third party like yourselves to do that for them? How does that work?

Elissavet Grout: Travers Smith

I think there’s a variation in the market. Of course, we would always be very happy to go. And we do, in fact, go to our clients and help them explain the benefits of the plans. And, you know, also how you should behave and what could create a situation where you would lose the benefits. So everyone is mindful of that. There are lots of other platforms out there. Some are using a lot of tech and AI as we all should to help communicate the benefits. There are a lot of frequently asked questions and answers that people can produce and give to their employee population. And I think it isn’t, you know, it is fundamentally a lot of the conditions are, I suppose, for businesses to be mindful of. They don’t need to explain them in too great length to the employees. But the employees do need to have their expectations managed in terms of, you know, what it is that they’re getting when they can realise value from it. And that’s the case with all options, not just EMI options. It’s that kind of understanding of what have I actually received and why is it good for me? When am I going to make money from it? You know, when am I going to benefit from this? So there’s a commercial discussion even before you get into the technical nature of EMI and the tax benefits of EMI. There’s a more of a commercial kind of understanding of what it means to have an option. And yeah, presentations, Q&As, one-on-one sessions. Sometimes our clients would like us to have those with employees. Also very happy to do that. So it really does depend on the employee population, their level of sophistication and understanding. And to be quite frank, their interest in learning more.

Marc Harris: BusinessTV

Thanks for clarifying that. And I know you as a firm have done hundreds of these, so you’re well skilled at advising individual companies on those communication channels and being able to help them with it as well. And I mentioned in my introduction, one of the reasons that we were so keen to speak with you, of course, is because of the recent expansion of EMI schemes in the budget now passed in November. A rare bit of good news to come out of that budget, but it’s meant now that more companies are going to be able to qualify to be able to offer enterprise management incentives. So can you take us through what really what that means from companies perspective? How is that going to affect other businesses that previously weren’t qualifying? Just your general take of things and where you think the market is going and what sort of companies are now going to be able to take advantage of this?

Elissavet Grout: Travers Smith

Yes, absolutely. And you’re absolutely right. It was a rare bit of good news, but it certainly was good news and we were all very happy to see this. And over the years, ourselves and other law firms in the city and across the UK have been lobbying for changes, more beneficial changes. So we were very pleased to see these. So to start with the independence test and the trading activities test that I mentioned at the beginning of our talk, those haven’t changed. So those are still fundamentally a requirement. But in terms of other good news, as I said, originally EMI was introduced for startup and growth companies at a time when we were part of the EU and there were state aid considerations that the government had to be mindful of. And so there were certain thresholds that you couldn’t breach. You would cease to qualify if you breached. One of those was a gross assets test. So as a company or group, you had to have fewer than 30 million gross assets. That test now has quadrupled to 120 million. So immediately bringing in companies with larger balance sheets into the equation. Similarly, it originally used to be that you had as a business fewer than 250 full-time equivalent employees. That threshold now has doubled to fewer than 500 full-time equivalent employees. And again, that gives a lot more flexibility to what type of business you are that can bring in EMI options. There was an overall limit to the number of options a business can grant at any one time to its population as a whole. That used to be 3 million pounds worth calculated at the time of grant of the options. That’s now doubled to 6 million pounds worth of shares calculated at the time of grant of the options. So again, you’ve got a larger, more employees, obviously a larger pool, overall pool to grant with tax advantages. Very good news. And it used to be the case that in order to get these tax benefits that I’ve been talking about, you had to exercise your EMI option within a 10-year window. And sometimes that wouldn’t be enough, because some businesses don’t come to a liquidity event within those 10 years. So they might not have found a buyer or they might not have come to the public markets in time. That period now has been extended to 15 years. So it gives you more time to grow your business before a liquidity event. And it means that you’ve still got qualified EMI options up until that point. Now, obviously, even 10 years, it’s not that common that people stay in the same business nowadays. But still, it’s better to have 15 years available to you than 10 years. So those are all really good changes and we’re very happy. What hasn’t changed, though, and it is worth mentioning this. So as I said, the independence test, not changed. Trading activities test, not changed. And the value of EMI options that any one individual can have at any one time in a three-year period, in fact, has not changed. And that’s £250,000 worth of shares at the time of grant. So that limit remains the case. So each individual can’t have more than that in a qualifying option. Obviously, they can have non-qualifying options that exceed that limit. But that hasn’t changed. And whilst we are lobbying, discussing whether that limit should be changed, and we think that government is thinking about it, it hasn’t changed for now.

Marc Harris: BusinessTV

Do you know why that wasn’t done earlier? Because it seems like it’s not an incremental increase, is it? It’s quite a leap.

Elissavet Grout: Travers Smith

Yeah, I suspect it did have something to do with the state aid rules so that you couldn’t grant. So state aid, you know, you can’t grant benefits that are too favourable to a particular industry because then it becomes anti-competitive. So that probably was part of it. But also, you know, it’s a giveaway. It’s a tax giveaway at a time when the tax authorities are looking to recoup revenues and bolster their tax revenues. So, you know, it’s a maths game. They’ve obviously done the maths and feel that it is important to give these benefits to a larger cohort of businesses because it will drive growth and it will improve businesses’ position in the market when they’re competing, not just within the UK, but obviously globally. So it was a bit of a surprise, but we’re very glad it’s been made. And what we’re hearing is that this is part of a greater emphasis on, you know, how can we support businesses and entrepreneurs in growing the UK economy?

Marc Harris: BusinessTV

Will those larger, more established businesses be interacting and using EMI in the same way that smaller businesses have done historically? Will their motivation for getting involved with EMI, is it more or less the same, or do you expect to see differences in how businesses approach EMI?

Elissavet Grout: Travers Smith

Sure, yeah, no, that’s a good question. So I think, you know, in very broad terms, you can probably separate out companies that offer EMI options maybe into three groups. So you’ve got your very small classic startup. Values of shares are very low. Stock options are cheap to give out because, you know, and money and cash flow is tight. You’ve then got a more established private company, but that’s still very broadly held. So it doesn’t have a controlling corporate shareholder. Those companies and the startups, they’re all looking for a liquidity event, right? So there isn’t any natural ability to sell shares when you hold them. And also there’s restrictions on selling them because they don’t want to have, you know, Joe Bloggs being a shareholder in their business. They want to have some sort of control over who their shareholders are. So those two groups typically will put in place what we call exit-based EMI plans so that the trigger for exercise is a liquidity event, such as a sale or an initial public offering on a public market. Management buyout, secondary investor coming in, something that releases cash so that you exercise your option and then you immediately sell the shares in the liquidity event and you realise value from that. So those companies are in those groups and I don’t think they’re going to change their behaviour, even though more companies in the private space will be able to take advantage because these tests have increased so they’re not worrying about their gross assets anymore or how many people they have in their business. They’re a bit more flexible. Where we’re going to see some perhaps different activity, and then you’ve got a group of companies that are already on the public markets, so in particular, AIM companies who could, who used to be able to grant EMI options. There were some with a small amount of gross assets. Now there’s going to be more of them and those companies don’t need to wait for a liquidity event. They don’t need to wait for an exit. They already have their shares on the public markets so they might behave in a different way where options are granted with a three-year vesting cycle, which is quite common in the UK. And then after three years, it’s up to the individuals whether they want to exercise their options and sell them in the public markets. It’s not always perfect because not all AIM companies are particularly liquid. So there’s still, companies need to think about the levels of dilution, the number of options they’re granting to people and how they’re going to manage that process. But they will behave differently. They will not be waiting for an exit to happen. They’ll be behaving more in a public company, listed company share option type way, but with great benefits from a tax perspective. So in many ways, it’s a win-win for those AIM companies that can now take advantage of this regime.

Marc Harris: BusinessTV

Let’s talk about then the sort of the key building blocks that a well-structured EMI plan must have in place because of course, obviously listening to you explain how things work. I mean, it does depend on the organisation where they are, what size they are, whether they’re listed on the AIM or not, what their aspirations are, when they think they’re going to have a liquidity event. So I suppose when it comes to structuring those options, the EMI schemes, the devil’s in the detail as it were. That has to be got as quite critical to get that right. So are there sort of certain pillars that you always look to advise your clients that they need to have in place with their scheme or certain key considerations that they need to be aware of?

Elissavet Grout: Travers Smith

Yes, so it’s kind of a running joke that even though EMI was brought in for the start of founder led companies, it is probably one of the most complicated tax favoured arrangements that you would ever have to put in place and the one that does require legal advice and valuation advice more than perhaps others. So unfortunately, that means that we often come to see quite a few problems that arise and situations where people thought they had qualifying EMI options and actually, it turns out that they don’t. So the way we would tackle this and other advisors would tackle this is the starting point would be, you know, do you qualify? Are you independent? Are you doing the right trades in order to qualify to grant EMI options? There is a process with the revenue where you can apply to ask for advance assurance, they call it. So you can write to the revenue, explain your share capital structure, the rights that your investors have in case they have any stepping rights or controlling rights, and the trade that you undertake and you know, your balance sheet to show your gross assets and all of these things. And the revenue will reply between two to four weeks, maybe six weeks time and say, yes, we agree based on what you’ve presented to us that you are a qualifying EMI company. We would recommend doing that as step one, because it’s helpful on an eventual exit, if you are a private company, and there’s a due diligence process, it’s helpful to be able to show that you’ve done that because that ticks the box for a buyer’s advisors. Once you’ve gotten over that hurdle, you then need to think about the structure of your plan. And again, EMI is the only tax favoured plan that’s very prescriptive, it has to be granted by way of a written agreement. And in that written agreement, there are certain things that you have to specifically say, including you have to say that it’s a qualifying EMI option pursuant to the relevant legislative provisions. And that sounds slightly crazy, but it has to be in there. And then there are other things in the EMI option agreements that you have to say or you have to put in place. And so yeah, you would need advice in order to ensure that the agreement you’ve prepared is EMI qualifying, and it hits all those necessary conditions. The other point that you would need to get advice on is the valuation exercise. So we talked about the tax benefits, the capital versus income. In order to get capital treatment, you have to have an exercise price for your EMI option that is equal to the market value of the underlying shares on the date of grant. And usually you can’t agree values with HMRC in this space, but for EMI you can. And so again, we would recommend you go to the revenue and agree the value of your shares for the purposes of granting EMI options, so that you have certainty of the tax treatment going forward. The key takeaway here, though, is that it’s not a legal obligation to get the valuation. And equally, you don’t even need to have it before you grant the options. So it shouldn’t, if you’re in a bit of a bind, and you need to act quickly, you don’t necessarily have to wait for the valuation to come through. But there are implications to the tax potentially, if you grant first, and then the revenue say, actually, we disagree with the value you’ve chosen, and we think it should be X. It doesn’t disqualify the EMI option, but it alters the tax treatment. So valuation is a piece. There’s a form that the revenue asks you to fill in, it’s relatively low key, you don’t have to go out and get an expensive valuation from a third party. But you do need to disclose a lot of information about your business. And one of the things you have to disclose is whether there’s been an approach or an offer to buy your business, because that alters potentially the value, obviously. And so as long as you’re fully, you know, upfront with the valuation team at HMRC, typically, their valuations can be quite generous, they can give quite large discounts to companies who are looking to grant EMI options. So valuation is key. So you start with advanced assurance, do I qualify? Am I independent? Am I trading? Am I meeting the gross assets test? Valuation of the shares that you want to grant options over a well drafted option agreement that is signed by both parties, both the company granting the option, and the individual accepting the option. That’s kind of the three step process. And after the fact, you have to then register your plan and notify the grant under an annual return. And there’s some changes in relation to that in years to come. But for now, just it’s just to highlight that there is a filing, reporting and filing obligation in relation to EMIs. So those are the four things I would say, is how to approach it.

Marc Harris: BusinessTV

And I take it you and your team, Elizabeth, are holding your client’s hands through that process. It’s starting, my head is spinning, it’s starting to sound really quite complicated. And I can imagine lots of viewers out there will be thinking, well, I will need help with that, because it’s critical that I get it right. But that’s your bread and butter, isn’t it? That’s why your clients are coming, or one of the many reasons your clients are coming to you.

Elissavet Grout: Travers Smith

Yes, absolutely. It is our bread and butter. And in a very simple scenario, it’s probably quite easy that we can equip businesses to do it themselves, or we can help teach them how to do it themselves. I think where we add the particular value is if there’s a there’s a concern over the independence test, or there’s, you know, there’s uncertainty around the trading activities, or there’s something in the background, a potential sale or offer that could impact whether or not you get the qualifying treatment. And that’s where we can particularly add value because we can, you know, navigate not only the legislation, but also the way in which HMRC practises and gives guidance on these points. And, you know, we can, we can give a good view of what we think the revenue are going to say about any particular situation that might be slightly out of the ordinary. So yeah, we can definitely help and equip businesses to get their EMI plans up and running. And in a plain vanilla scenario, we would hope to set our clients free to be able to do it themselves. But there are certain points where actually legal advice can really save some money and really kind of guide a business into a way that’s much more beneficial to them than the perhaps they might otherwise have thought.

Marc Harris: BusinessTV

Working with a firm, with Travis Smith, you and your team, a lot of the advantages for the clients is that you’re able to help them shore things up from a legal perspective, so that what’s being written down, ultimately, is watertight. And of course, at the same time, you’re creating a paper trail to that whole process, aren’t you? So if at any time point in the future, something does need to be argued in the favour of the company, everything is everything has been clearly laid out and a rigorous process has been has been adhered to at the outset. So I think that’s, I think that’s very important. Are there any situations where you have seen a case where a scheme hasn’t been well thought through in advance, and then that has, that has perhaps even scuppered the ultimate goal of an exit or an IPO or a sale of the business, because of a badly thought through EMI scheme? Has that ever happened? Does that happen?

Elissavet Grout: Travers Smith

Yes, and you know, I think badly thought through is probably a bit mean, because, you know, it’s, you know, when you’re in the start, it’s very difficult to kind of contemplate and apprehend what might happen in the future. And, you know, market, the markets and the economy, that it’s so volatile, at the moment, things change, and the way in which you thought you might operate changes. But I would say that what we see that the biggest difficulty we have is if we have a client that comes to us, this is great, we’re going to sell our business, we’ve got all these EMI options, everyone’s going to make a lot of money, and everyone’s really happy about it. And it’s all going to be capital gains tax, isn’t it? And when we drill down into the detail, typically, a sale to a third party, so a change of control is likely to be a trigger event for exercise. So that should be okay. But we have seen plans which have provisions in them, which say that, you know, if this if the founders or a large proportion of the existing shareholders continue in the business going forward, that doesn’t constitute a sale. And we know that it’s quite common that a buyer when they come into a business will want to tie in the exiting shareholders will want them to roll over into the business. So you can see there might be a disconnect there between what the rules say about well, when you can exercise your options, and what commercially is most likely to be the ask of the buyer coming in saying, Okay, yeah, you are going to make a lot of money, we want you to reinvest quite a bit of that into our equity, you know, because we think you’re important to the business, and we want to continue the business. But that’s one thing that sometimes comes up. The other thing that comes up is that it might not be a sale of a controlling interest, it might be a minority, a sale of a minority interest. And the founders might say, we’re going to sell 30% of our shares to this new investor. And we would like our option holders to have the same opportunity. And often, exit place based EMI plans do not trigger exercise at a secondary minority investment. So then you’re saying, well, unfortunately, you can’t bring your option holders along for the ride on this, unless you accept that they will lose the tax treatment of the favourable tax treatment of their options, the ones they choose to exercise. Thankfully, I think we’ve had HMRC confirmed that to the extent that you don’t exercise some of your options, you could probably continue to keep them in the EMI qualifying world. But if you do something outside of the terms of the option plan, there’s no saving you, you can’t really go to the HMRC and plead your case, because they can be quite strict around, well, you didn’t have the right to exercise in this scenario. So if you choose to, you’re essentially breaching the EMI contract, it no longer exists in relation to those options. We’ll have all the tax, thank you very much. So that’s a, you know, minority investments and trying to bring your option holders along for a, like a sell down, a partial sell down, partial liquidity, often becomes a problem, because that’s not contemplated at the time the scheme is put in place. And then rollover reinvestment and have you actually exited the business in the way that the plan envisaged that you’d exit the business is another thing we we see. And the third thing I’d say is if you are, if you are being looked at or bought out by a US company, a US buyer, they tend to prefer to cancel options in return for a cash payment. And with EMI, if you do that, you will lose all the tax benefits. So when you’ve got overseas, in particular, US investors and or buyers looking at your business, you need to, you know, educate them in the EMI rules, and why you will need all your option holders to exercise their options, acquire set shares, and then sell those shares to the US buyer. And in the US, that seems completely counterproductive and anathema to why, why wouldn’t you just cancel everything for cash, but you know, you’ve got to stand firm on that, because otherwise you will lose, you will lose your tax benefits.

Marc Harris: BusinessTV

Right, I see. I suppose unless the US firm is prepared to pay an absolute premium for the, for the…

Elissavet Grout: Travers Smith

There’s no need, once you’ve explained it to them, they normally understand, but their starting offer will be, oh, let’s cash all of these people out, that’s much easier than getting them to sign an SPA and sell shares, you know, it makes sense. It’s just it disqualifies the tax. So it’s, it’s a point that we should be live to if we’re looking to US.

Marc Harris: BusinessTV

Does the, does the valuations make a difference then to the long term success of an EMI scheme?

Elissavet Grout: Travers Smith

So, so we touched upon it a little bit. So valuation is key because you want to set your exercise price at an equal to the market value of the underlying shares. Yes. There’s also your limit, the limits I discussed, so you’ve got an annual limit of £250,000 worth of shares and an overall limit now of £6 million worth of shares. So you need to know that you’re operating within those limits. And it gets a bit techy, but the exercise price is market value, the limits are unrestricted market value. So ignoring any restrictions attaching to the shares in terms of forfeiture, or transfer restrictions. These are a bit technical, but HMRC will typically be quite generous with the with the market value. So you get a low exercise price, which is helpful. But yes, you need to get a valuation of both the market value and the unrestricted market value so that you can operate within the tax rules plus the limits that apply to EMI. And again, an advisor will be able to navigate that for the business and explain the differences. And then the other point in time where valuation might be key, and we’ve not talked about this is, well, what happens if I had an option that was qualifying, but I then something happened and it disqualified and the most obvious disqualifying event, which is the language we use, is someone ceasing to be an employee. Because EMI really is about recruitment and retention. So you’re working in the business driving it forward. If you leave the business, then that disqualifies the option. You have a grace period of 90 days to choose to exercise, at which point you wouldn’t get any adverse tax treatment. But if that 90 day window passes, and you’re still allowed to keep your option, which is fine, you can, you then from that point onwards, from the point of the disqualifying event, all the growth in value from that point onwards, is subject to income tax on exercise. And the growth whilst you were qualifying whilst you were in the business is subject to capital. So if you have a disqualifying event, you might need to record at that point, well, what was the value of the shares at this point in time, because that’s going to be an issue when this person in the future exercises their option, I’m going to need to know that to calculate the tax liability for this individual. That doesn’t need to be agreed necessarily. But it just needs to be because often we see companies going, oh, we had loads of people leave, but we’ve let them keep their options. And we said, well, what was the value of the shares at each point in time? And they’re like, we don’t know.

Marc Harris: BusinessTV

Assuming sales or exit plans go through smoothly, and they’re fairly straightforward. And therefore, there’s nothing to derail an EMI scheme in that respect. Are there any compliance or administrative issues that can raise their heads after an EMI scheme has been implemented, that again, companies should be cognisant of or that you advise your clients that they should be aware of?

Elissavet Grout: Travers Smith

I think the things that can come up, so obviously, we’ve got, as I mentioned, there’s filing and reporting obligations. So you have to be on top of those. They are a little bit admin heavy, but there are penalties if you fail. So you really should be on top of those. The other point to think about is that if you’ve granted EMI options in the last 12 months, and you then sell the business within that 12 month period, or very shortly afterwards, what we see the tax authorities do is kind of, if it’s something that’s published in the press, in particular, they will look at that and can try and connect the dots back and say, well, hang on a minute, you said the value of your shares was X, six months ago, and you came to us and said you wanted to grant EMI options and you granted them. And then you sold your business six months later at a value of Y, we think you didn’t disclose everything to us. Or that that valuation is not, and therefore that valuation is no longer valid or binding on us. And we think there should be more tax to pay. Now, we’ve had situations like that, we’ve written back to the revenue said, listen, it was absolutely unexpected. We asked you to value that we had no approach at that time, we had no idea someone was going to come and buy us, it was totally unexpected.

And they might accept that, you know, oftentimes they do accept that. But if not, if there hasn’t been a kind of the proper, you know, disclosure to HMRC, then it can become a little bit awkward trying to defend the position. And in an exit context, people would have given indemnities, and they would have given warranties. And so then you’re thinking, okay, if we can’t successfully convince HMRC of our position, and there’s extra tax to pay, how have we apportioned that in this transaction? You know, is it the selling shareholders that bear the brunt? Is it the selling option holders that bear the brunt? Is it the buyer that’s bearing the brunt? So, you know, in an exit liquidity event situation like that, there will be a lot of thought on what happens if, through the best will of us all this EMI plan is challenged by HMRC. And, you know, I will say it doesn’t happen that often, you know, you know, they’re not, EMI isn’t the one where they’re going after people all the time. But it does happen sometimes, especially if something makes a big splash in the press, and the values are high, it does make them think and go, Oh, hang on a minute, you know, this, this company was granting EMRC not that long ago, have they told us everything about it? Have we done the right thing here? So that’s just, you know, anecdotally, my experience, but with AI as well, and all the other tools that the revenue authorities are going to have at their disposal in the years to come, they will be connecting the dots, and they will be using hindsight. So it’s always good to be prepared.

Marc Harris: BusinessTV

Yes, and they’ve got a lot of data, I’m sure they’ve got a huge amount of data at their disposal, that gives them a general indication of after, when a scheme has been set up, typically how long it takes for a company then to, you know, to exit or take their business to fruition. And obviously, if there’s a very obvious anomaly, then that might well raise a query, mightn’t it? So yeah, what sort of what sort of companies, again, you’re talking anecdotally, but of course, you’ve got a huge amount of experience in this area. I know that you’ve done hundreds of these when one of the most prolific companies operating in this area. What sort of what sort of companies, ownership structures, businesses, goals do you see tend to tend to work best with EMI schemes? Is that is that a fair question? Do you see any common denominators between companies who are who are entering into EMI?

Elissavet Grout: Travers Smith

Other than the, as I mentioned, at the beginning, the expectations of certain industries, particularly the tech and fintech industries, if possible, of just having stock options, you know, and that’s come across from from the states. EMI, you know, the UK has a lot of it has got a quite well established share plan regime, generally speaking, so it’s all very clear what you have to do in order to get into a particular regime. And it’s all very clear how you’re taxed on all all types of employment related shares and share options. And the US is relatively similar. There are other overseas jurisdictions like France and some of the Eastern European jurisdictions which are trying to pull together favourable stock option regimes. And in fact, there’s an EU wide initiative to perhaps come up with an EU wide stock option arrangement. And they’re looking at EMI as an example of what works well in the UK, so that businesses who are attracting talent, and competing with talent on basically on a worldwide scale have are able to grant stock options with favourable tax provisions. And, you know, the EMI, not only is it the capital rates, but it’s also the fact that tax, if you’re in the capital regime is deferred to the sale, so it’s deferred to the liquidity event. So what you want to avoid, all these companies want to avoid is a dry tax charge, a tax charge arising before you’ve made any money from your option, because then you’re putting your own money at risk, you’re paying tax, which you won’t get a refund for most cases. And you don’t know if you’re actually going to make any money from the underlying shares. So the common goal of all these businesses putting EMI in place is getting the capital rate, but also deferring the tax to a point in time when people are going to be liquid. Those are very key. And the other one is because you don’t have to ask people to make an investment upfront. And that might be counterintuitive, because some businesses want people to have skin in the game, they want to ask people, certainly senior people to make an investment in their business. But I would say, once the capital treatment is explained, that kind of in many ways, trumps that requirement, because it’s so much more favourable to both employee and the employer to have an EMI option that is qualifying. The other things that companies in this space can do is often a share ownership arrangement or grow shares or hurdle shares, they are very costly, and more complicated because they require an amendment to articles and shareholder agreements, which typically if you have more than a handful of shareholders is a real pain to kind of open up, go and get consents for explain the commercial rationale as to what you’re doing and why you’re doing it. So, you know, EMI, you know, the driver is not necessarily sector specific, as long as you meet the conditions, it’s more the fact that it’s, it’s just so much easier and so much more tax favourable than anything else that’s available.

Marc Harris: BusinessTV

And important to note, or to mention that, of course, while you’re you and your team are experts in EMI, if for whatever reason, it’s not the best route for a client, and you’re able to work with a client and sort of understand their goals and aspirations and structures, etc, and advise them, you also advise on lots of other types of employee share scheme options, don’t you? I mean, you’re able to advise your clients on on whatever, whatever option is best for them.

Elissavet Grout: Travers Smith

Absolutely. And we would always give, you know, an option of different types of arrangements that might be preferable. Sometimes people think, you know, cash settled arrangement might be of more interest. If you’re a business, you know, for example, a lot of the utility companies or, you know, infrastructure sector is a long, you know, businesses are held for the long term. So actually, you know, you’re not looking for an exit, you’re not looking for, you know, a liquidity event that requires a purchaser to come in, and you might then be cash rich, and you might be happy to be paying cash out to people. Now, you’re not going to get the benefits of the capital treatment, but it might just be a more simplified route for you. So we wouldn’t push anyone into EMI, we would make sure that they understand what alternatives are available, the pros and cons of each. And then our clients make an informed decision based on that. And as they grow, and if they’re unable to meet even the now enlarged limits and conditions, we then can discuss well, what’s the next available arrangement, there’s the company share option plan, there’s grow shares, hurdle shares. And then there are some other all employee plans, save as you earn or share incentive plan, which might be adopted alongside or as an alternative once you’ve grown a bit more for your wider population. And we also we also advise a lot of overseas companies with businesses in the UK, because the requirement is that you have to have, at a minimum, a permanent establishment in the UK. So an entity that pays corporation tax in the UK, you don’t have to be UK incorporated company, you don’t have to have a subsidiary in the UK. So there are overseas businesses that often ask us, what’s the most favourable thing we can do for our UK people. And EMI often comes up as something that overseas businesses also want to adopt in the UK.

Marc Harris: BusinessTV

When should individual business owners get in contact with you and your team? Elizabeth, when is it? When does it make sense for them to spark up a conversation with you? And why? I’m assuming is it important for people to start to bring you in early in the process as opposed to later?

Elissavet Grout: Travers Smith

Yeah, I mean, you know, every business is different. But as we’ve discussed, the valuation is important. Obviously, the if you’re doing this at a time when your values are low, it means people will obviously have a greater opportunity to, to gain and grow. So, you know, there’s never a right time, because you’ve got to commercially be in the right place. It may be though that if you are looking to attract talent, and you’re struggling to do so, it may be that it’s because you’ve not offering the full gamut of what, you know, people in your industry are expecting. So at that point, you might want to think, well, I want to be able to offer something in my recruitment strategy to people, I don’t know how to phrase it, you know, you’ve got to be careful what you promise people, right, because these are legal obligations. So then, at that point, I would recommend getting some advice, we could even just help, you know, frame, you know, a paragraph or two of what the company might be putting in place in the near future, in order to attract people, even if they don’t have a plan right now. Because we do see situations where people have promised a lot of things, and then they can’t be delivered. So that, you know, there’s a, there’s, there’s some advice to be had there. And well, how do I maximise what I can offer what I want to offer to people and, you know, enhance that recruitment process, when you’ve got people that are established in your business, and they’re looking to you and saying, look, we’d like a part of the equity, you know, again, that’s a good time to talk to legal advisors, because we’ll talk through, is the EMI plan, right? How much equity Are you happy to give away? What do you want the terms and conditions of that giveaway to be, you know, the world is your oyster in many ways. So it is helpful for us to have those conversations with clients. Because we’ve seen what happens in the market, we can then have, you know, we can then say, look, X, Y, and Z are quite common, but you might want to think about this, if this is important to you. So it’s a two way conversation. It’s not a black and white situation where, you know, everyone does one thing and the same thing. So that’s where advisors can can be very helpful. And then in the background, we’ll be doing the heavy lifting with making sure all the legal positions are ticked, or the admin is signed off, you know, all of the things that are boring and technical, we can deal with, but the commercial discussions, we’re particularly good at because we’ve seen plans designed, we’ve seen them operated, and we’ve seen them essentially pay out. So we know what happens at each stage of the life cycle.

Marc Harris: BusinessTV

As you said, having a having a commercial overview of what works as well is all is important. I wanted to ask you just quickly, is there, from a company owners perspective, is there any jeopardy involved when deciding which employees are going to be on the receiving end of this? Is it something that companies tend to try and keep quiet within who to whom they’re offering them to? And is that is that a difficult? Is that a difficult process for companies to navigate? And do you help them with that?

Elissavet Grout: Travers Smith

Yeah, I mean, obviously, from a legal perspective, we include all the usual statements, this is confidential, only disclose it to your close family and your, you know, advisors. And but it depends on the culture of the business, right? Because people talk to each other. And you know, it’s very hard to stop people from talking to each other, right? And I think the biggest issue that businesses face, the biggest kind of risk that businesses face is while not having well drafted leaver provisions, so not having a clear understanding of what happens if someone leaves, because, you know, when everyone’s happy and getting along, that’s not something that people want to focus on or think about, but actually, it things can go wrong, and people can fall out. And, you know, you then think, Oh, gosh, well, I don’t want this person who’s now I’m not happy with their performance, or I’m not happy with their behaviour to walk away with some of my stock that, you know, that seems anathema to me. And yet, I didn’t really, you know, plan properly for the situation. And equally, you know, you’ve only got a finite pool of equity that you’re prepared to give away. So if you for whatever reason, someone moves on, you’ll want to recycle their allocation, you won’t want them to take their allocation with them. And then you have to find a more equity to give their replacement. So it’s very important to think about, you know, I love these people, I want to give them these benefits, but I really should prepare for what would happen if they were to leave. And I need to be quite clear on that, that this is a retention recruitment tool. I need to think about, well, yeah, is there a good leaver scenario that I’m prepared to allow people to keep some stock? Because, you know, typically death obviously is not very common. So that’s, you know, something that you can be quite generous with. But other situations, you know, people go to competitors, all of these things, you’ve got to be careful, you’ve got to thought of them, even when times are good, and everyone is happy.

Marc Harris: BusinessTV

Any, any other sort of key pieces of advice that you would give potential EMI adopters?

Elissavet Grout: Travers Smith

Yes. Yeah, I would say that, as I say, it’s a great benefit, but don’t immediately go to EMI to the exclusion of all other arrangements, because it is a good, you know, you should really have a good understanding of what the landscape looks like in the UK before you pick EMI. And if you are a business that has overseas employees, you know, you might want to try and find an arrangement that fits better for everyone or not, you know, these are these are choices that you have to make ultimately. But yeah, you might want to think about, well, do I use the EMI as my template for what I might do in France, Spain, Italy, America? Or do I try and find an arrangement that fits everyone better? That’s something to think about. I think EMI works well, on its own in the UK. But if you’ve only got one or two people here, and more important people elsewhere, then you might be spending too much time contorting yourself into an EMI plan when actually your important people are somewhere else. And then the other thing I don’t think we mentioned, again, yet another condition, you can’t give EMI options to non-executive directors. And we do often get questions around this. And, and the reason for this is predominantly because, you know, even if you were to put them into an employee situation, there’s a working time requirement to qualify for EMI as an individual, which is 25 hours a week, or if less, 75% of your working time. So really, if you have a number of different roles in more than one business, the company in which you’re getting an EMI option has to be 75% of your overall working time in all businesses. So, you know, so non-executive directors currently don’t qualify. And we do get sometimes questions around this. Consultants don’t qualify, other service providers that are engaged with you, perhaps through an intermediary, like an agency, or an employer of record, or anyone that isn’t really in your group of companies, they will not qualify either. So, you know, just, there’s a lot of different ways in which people can engage their staff, including very technical and key staff. But it’s just bearing in mind, they won’t have EMI qualifying status. So anyone who’s a consultant, non-executive director, agency worker and the like.

Marc Harris: BusinessTV

Elizabeth, thanks very much for taking us through EMI. I mean, of course, viewers out there, obviously, as you will have learned through this conversation, it’s a nuanced topic, there’s lots to consider. So it’s really important to get it right. So please remember that you’ve got lots of mechanisms below this video as it plays on your screen that will enable you to reach out to Elizabeth and her team. There’s a great form there that you can fill out, it only takes a couple of seconds to do so. And we’ve got lots of deep links through to Travis Smith’s website, where you can travel through to various different pages on their website to learn more about EMI, learn more about what they do as a firm, how they operate. And so please take advantage of all of that. Elizabeth, thank you very much for joining us. Thanks for taking us through the topic. I know there was probably a million other questions that I could have asked you. It’s a very complicated topic, but in principle, I think we all understand it. But thanks very much for sharing your time with us today.

Elissavet Grout: Travers Smith

My absolute pleasure. Thank you, Mark.

Marc Harris: BusinessTV

Thank you.

Please get in touch with Elissavet and her team using this form

Elissavet Grout – Partner

Tax Incentives and Remuneration Group

Elissavet has considerable experience in advising on the incentive and remuneration aspects of corporate transactions such as management buy-outs, IPOs, takeovers and mergers. She also advises on the design, implementation and day to day operation of all types of tax favoured and unapproved equity incentive plans. Elissavet is a specialist in global mobility and employment tax queries both in the context of share incentives and remuneration arrangements more generally.

Elissavet has strong advisory relationships with many AIM and Main Market listed companies, as well as large private companies and notable asset managers.

Elissavet is a member of the Share Scheme Expert Group of the Quoted Company Alliance (QCA) and the Share Plan Lawyers Group. Elissavet participates in many of her firm’s corporate and social responsibility initiatives, such as ‘Legal Experts in School’, and regularly contributions to the firm’s pro-bono workstreams.

Most recently, Elissavet spoke at the 7th Annual International Tax Congress on ‘Navigating Tax Challenges in Global Mobility’.

We know each other well and we know that we get the best results when we act as a team – not just within our legal teams, but right across our firm where we welcome diversity of thought and views from everyone. This is our difference and we are proud of it.

Our clients know that we treat their business as our business, their dispute as our dispute, their challenges as ours. They know that wherever in the world they or their ambitions lie, we will work as one of their team to get things done. And they know that we do so in a straight-talking, thoughtful and open way. Read more…

Incentives & Remuneration

We want to help our clients achieve long term and sustainable business growth.

A key part of that goal is the retention and motivation of staff through effective incentive arrangements. Our Incentives and Remuneration team specialises in advising businesses on the design, implementation and operation of the right plan for them.

Executive Remuneration

Having the right remuneration package for key managers is vital to the success of a company.

However, balancing the need to attract and retain the best talent against shareholder concerns around value can be difficult.

Share Plans

Your employees are key to the success of your business.

Choosing the most effective and appropriate form of incentive plan can present employers with complex challenges.

ESG and Impact

Working with asset managers, lenders and companies in managing the operational, reputational and compliance risks associated with ESG and Sustainability factors, and seeking to make a positive impact.

Click on the postcards below for Podcasts & Videos from Travers Smith’s Experts